Trump 2.0's Potential Measures Against China – Four Tariff Scenarios

And China’s Potential Countermeasures and Strategic Adaptation

The return of Donald Trump to the U.S. presidency likely marks a renewed and intensified phase of U.S.-China economic and strategic competition although the Biden-Harris administration “completed” an unprepared Trump 1.0 and turned its coercive policies into a whole-of-government approach of containing China. Drawing lessons from Trump’s first term, however, a dominantly China-hawkish Trump 2.0 cabinet suggests the implementation of a broader and more comprehensive set of policies. These measures likely aim to exert maximum economic pressure on China by leveraging trade tariffs, realigning supply chains, and imposing sectoral restrictions to further constrain China's economic development or reverse it, as some in Washington DC hope. It also involves enforcing global reliance on the dollar by targeting China and other countries that seek to de-dollarize trade. This could further intensify U.S.-China competition, as China’s export-driven economy remains vulnerable to such coercive measures. According to Liu Yuanchun, President of Shanghai University of Finance and Economics, China can by no means hope for a “transactional Trump.” Instead, it must respond to a second wave of decoupling–one likely to be “faster, more profound, and more systemic” than that experienced during Trump’s first term.

While the first round of the trade conflict already inflicted visible economic pain on both nations, a renewed andintensified phase will highlight structural challenges within China’s economy. Still growing in 2024 at around 5%, China faces the "3Ds": dismal demographics, daunting debt, and deficient demand. All three are tightly linked to the collapsed property market, which accounts for an estimated around 30% of China’s GDP. Local governments face high levels of debt, officially reported at around 35-45% of GDP, but unofficial estimates, including off-balance-sheet liabilities like local government financing vehicles (LGFVs), suggest a total debt ratio of 75-91% of GDP. For comparison, the EU’s Maastricht Treaty sets a limit on government debt at 60% of GDP. These structural and cyclical factors, coupled with the necessity of transitioning towards an innovation-driven economy with focus on “new quality productive forces,” significantly constrain China’s ability to respond to the unilateral coercive measures of the Trump 2.0 administration compared to the Trump 1.0 era. For this reason, the government has introduced a series of economic stimulus measures to stabilize the economy and improve resilience. These include a substantial fiscal package of 6 trillion yuan (approximately $839 billion) to assist local governments in refinancing their debt burdens, cuts to mortgage rates, reductions in the reserve requirement ratio for banks, and a shift to a "moderately loose" monetary policy for the first time in 14 years. Together, these measures aim to bolster domestic demand, address structural weaknesses, social security, and provide some capacity to respond to the actions of the Trump 2.0 administration.

The following analysis draws extensively on calculations and insights presented by Professor Liu Yuanchun at the 2024 Dishui Lake Emerging Finance Annual Conference, held in Shanghai’s Lingang Free Trade Zone on December 6. Liu’s projections provide a detailed examination of the potential economic impacts of U.S. policies towards China under Four Scenarios, revealing both vulnerabilities and China’s adaptation strategies.

To summarize, the analysis reveals a stark asymmetry: China bears the brunt of trade disruptions, particularly in exports, imports, and social welfare, while the U.S.—though not immune to shocks—appears better positioned to weather the economic confrontation. The severity of Scenario 1 emphasizes China’s acute sensitivity to external trade measures, while Scenario 4 reflects the devastating long-term consequences of systemic decoupling. If Trump 2.0's goal is to inflict maximum harm on China and seek to isolate its economy while minimizing the impact on the U.S. economy, a combination of Scenario 1 and Scenario 4 is the most likely approach.

1. U.S.-China Trade Conflict: The Trump 1.0 Escalation

Let’s take a step back first. U.S.-China relations escalated significantly during Trump’s first presidency, as marked by the unilateral imposition of sweeping tariffs on hundreds of billions of dollars’ worth of goods, aggressive decoupling rhetoric, and a strategic shift towards containment of China’s economic and technological rise, especially targeting China’s 5G technology and initial restrictions on semiconductors, including limits on China’s access to U.S.-origin chips and software. The imposition of tariffs, the targeting of strategic industries, and export restrictions on technology created a framework of confrontation that continues to shape bilateral economic relations. The Biden-Harris administration expanded the extensive tariffs and restrictions on semiconductor exports and introduced broad measures in October 2022 to block China's access to advanced semiconductor manufacturing equipment and high-performance chips crucial for AI and military applications. As one of the final measures of the outgoing administration, in early December 2024, the U.S. Department of Commerce added approximately 140 Chinese technology companies to its Entity List, primarily targeting those Chinese companies involved in semiconductor production, chipmaking tools, and related software.

Despite the Biden-Harris administration expanding on these measures, it is essential to revisit the groundwork laid during Trump 1.0, which set the stage for these developments. Between 2017 and 2019, as summarized in Table 1, China’s export growth to the U.S. dropped dramatically from 11.3% to -12.5%, while imports fell from 14.5% to -20.9%. As a result, China’s share of U.S. imports declined from 21.9% in 2017 to 13.9% in 2023. Additionally, China's semiconductor import growth, which had been 19.8% in 2018, turned negative at -2.1% by 2019. The Chinese yuan depreciated by 11% against the U.S. dollar, while its effective exchange rate dropped by 6% during the same period. These measures, combined with the economic disruptions caused by the health pandemic, had a significant negative impact on China's economy. They exposed vulnerabilities in China’s reliance on external demand and highlighted challenges in diversifying trade markets to offset losses from U.S. policies with focus on ASEAN region.

At the same time, China managed to partially offset these losses by re-routing supply chains and expanding trade with other countries. Trade growth with ASEAN nations and other emerging markets increased by approximately 5% during this period, reflecting China’s ability to adapt to shifting global trade dynamics. These efforts, however, were insufficient to fully counteract the U.S.-induced disruptions, particularly in sectors reliant on American markets or advanced technologies.

These impacts laid bare China’s vulnerabilities, particularly its reliance on external demand and its struggle to diversify trade markets. The focus on ASEAN and other emerging markets was a clear response to offset losses, but the data suggests this pivot was not sufficient to fully mitigate the effects of U.S. policies. The combined effects of these measures weakened China’s trade position, heightened the urgency for domestic innovation, and accelerated efforts to reduce dependency on U.S. technology and markets. These dynamics set the stage for a more proactive Chinese strategy in subsequent years, including its push for greater self-reliance and expanded regional trade agreements like RCEP, which still is lacking momentum. However, they also highlight the deep interdependencies and vulnerabilities in global trade systems, leaving China exposed to further external shocks.

2. Four U.S. Trade Policy Scenarios under Trump 2.0

The Trump 2.0 administration, starting in January 2025, could rapidly adopt a range of coercive and protectionist measures against China, escalating from targeted tariffs to systemic policies designed to apply maximum economic pressure. According to a Reuters analysis, such measures could have severe economic consequences for China. Under a 38.6% tariff scenario, China's GDP could decline by 0.5% to 1.2%, and exports could fall by 8.1% to 55%, depending on the scale and duration of the tariffs and China's potential countermeasures. The economic impact would not be immediate but would deepen significantly in 2025, as quarter-over-quarter real GDP growth declines by up to 1.0 percentage points before showing signs of recovery in 2026. This decline stems from several contributing factors:

Net Trade: A sharp reduction in exports due to the tariffs would act as a primary driver of the GDP contraction.

Trade Policy Uncertainty: Uncertainty around trade policies would exacerbate economic pressures, disrupting business confidence and investment decisions.

Financial Conditions Index (FCI): Tightening financial conditions, including potential capital outflows or credit stress, would add to the economic slowdown.

Real Income: Negative effects on household income would further suppress domestic consumption, amplifying the downturn.

While Reuter’s estimates provide a clear warning, it is worth noting that the projections involve uncertainties, as outcomes depend on the scale of the tariffs, the duration of the measures, and China’s ability to implement effective countermeasures.

Professor Liu Yuanchun outlined four scenarios highlighting the potential severity of each strategy. The quantitative analysis is based on Global Trade Analysis Project (GTAP) modeling, a widely used economic framework that evaluates the impact of trade policies, tariffs, and economic shifts on global and regional economies, allowing detailed sectoral and macroeconomic assessments.

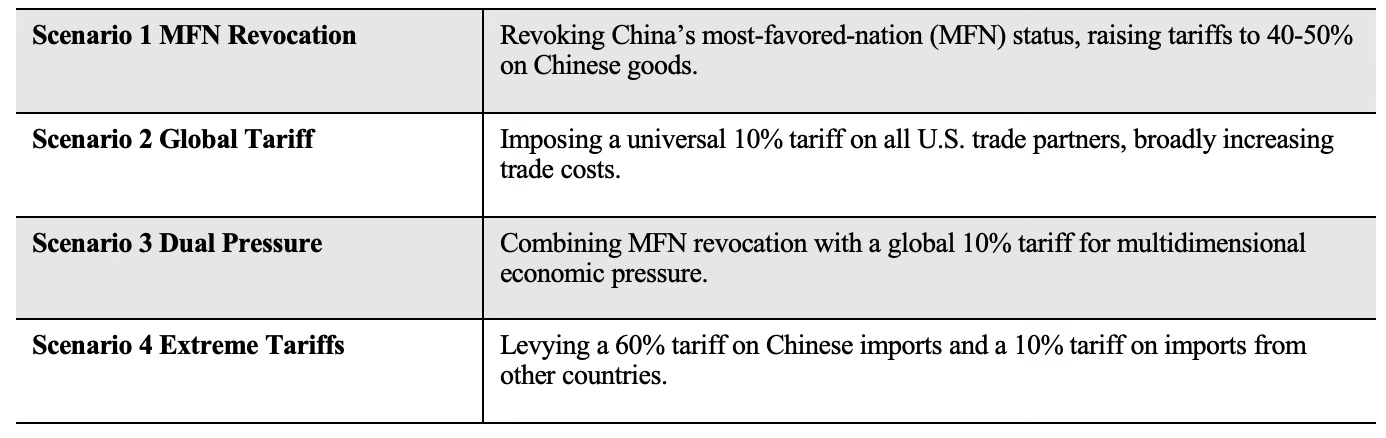

Scenarios 1 and 3 represent a targeted approach toward systemic decoupling by focusing on China’s Most-Favored-Nation (MFN) status. In Scenario 1, the U.S. unilaterally removes China’s MFN status, raising tariffs to 40-50%. While this appears to be a “milder” measure structurally, it disproportionately impacts China’s trade flows and social welfare, revealing the economy’s acute sensitivity to external shocks. In Scenario 3, this pressure is compounded by the imposition of a global 10% tariff on all U.S. trade partners. This dual approach amplifies trade disruptions while increasing inflation risks for the U.S., signaling an aggressive escalation of trade decoupling.

Scenarios 2 and 4 reflect a broader, protectionist strategy that bypasses WTO norms by applying universal or selective tariffs. Scenario 2 spreads the economic pressure evenly across all trade partners through a 10% global tariff, leading to higher consumer costs in the U.S. and moderate impacts on China’s economy. By contrast, Scenario 4 applies an extreme 60% tariff on Chinese imports, alongside a 10% tariff on imports from other countries. This devastates China’s export-dependent industries, particularly electronics and machinery, and inflicts systemic economic damage through sharp declines in GDP and social welfare.

Together, these scenarios reflect a fundamental shift from selective tariffs to systemic trade decoupling. While Scenarios 1 and 3 target China’s competitive edge more directly, Scenarios 2 and 4 escalate trade protectionism globally, using China as the primary focal point. Trump 2.0’s policies, therefore, represent an attempt to achieve U.S. economic realignment at the cost of fracturing global trade governance, further weakening an already dysfunctional WTO and accelerating a shift toward fragmentation and protectionism.

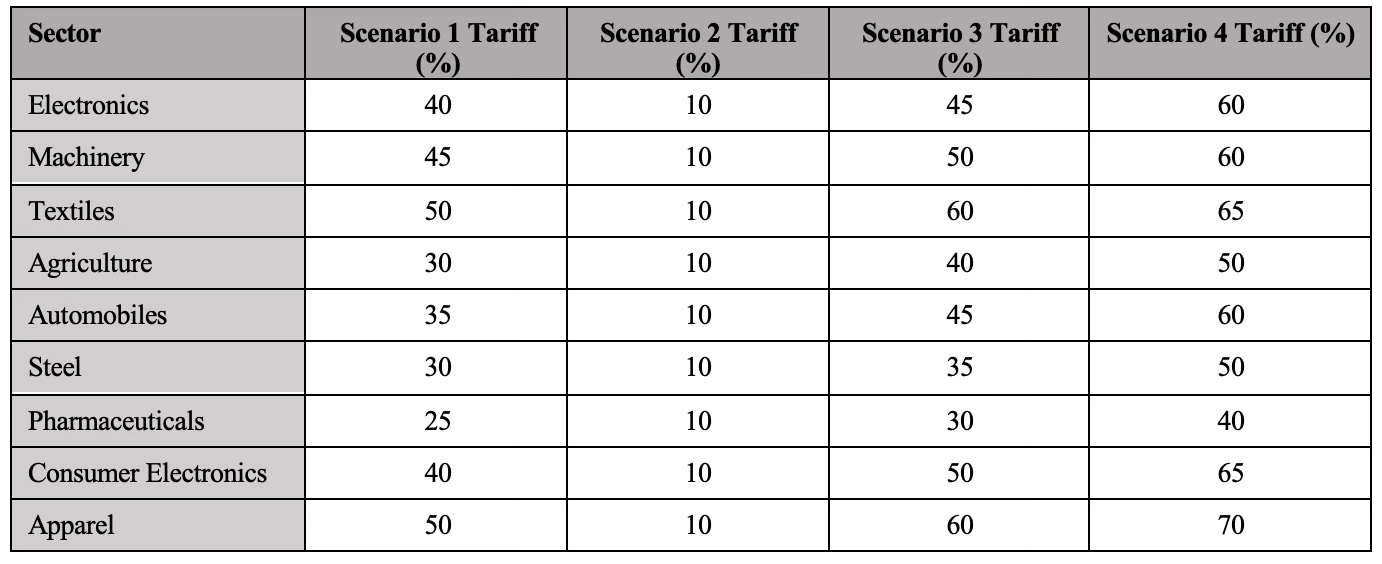

As shown in Table 3, the four scenarios assume varying levels of U.S. tariffs, applied across different economic sectors. To provide additional granularity, the table outlines sector-specific tariff rates under each scenario. These rates serve as the basis for modeling the broader economic impacts on GDP, trade flows, and social welfare. In Scenario 1, targeted high tariffs on critical Chinese export sectors like electronics, machinery, and textiles aim to disrupt China’s industrial competitiveness. Scenario 2 applies a universal 10% tariff across all sectors, diffusing the pressure globally but moderating its severity. Scenario 3 escalates the pressure by combining targeted tariffs with a global 10% rate, while Scenario 4 imposes extreme tariffs—reaching as high as 70%—to cripple China’s export-driven industries. The sector-specific tariff rates explain the significant declines in China’s exports and imports observed in the macroeconomic analysis, particularly in Scenarios 3 and 4, where trade disruption becomes systemic.

3. Key Macroeconomic Impacts on China and the U.S. based on the Four Scenarios

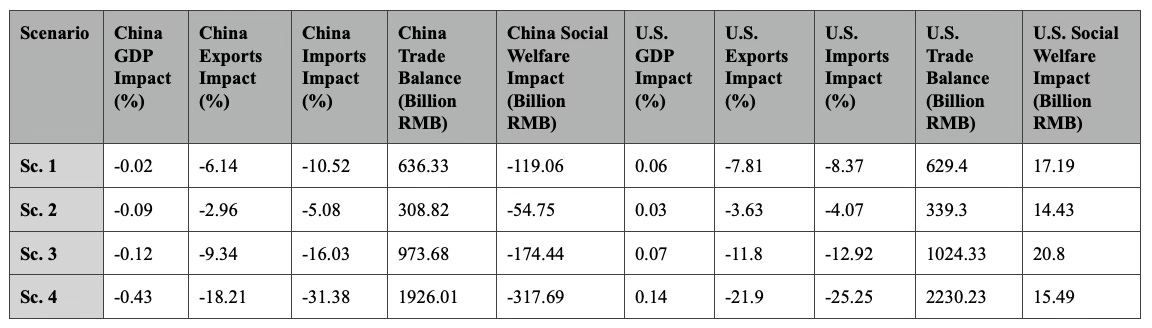

The following analysis evaluates the economic impacts on China and the U.S. under the four distinct scenarios outlined above. These scenarios have been calculated based on changes in five critical macroeconomic metrics: GDP, exports, imports, trade balance, and social welfare. As the scenarios progress from the least to the most severe, the impacts intensify, providing insights into which economy is hit hardest and by what measures. As shown in Table 4, the analysis reveals a stark asymmetry: China bears the brunt of trade disruptions, particularly in exports, imports, and social welfare, while the U.S.—though not immune to shocks—appears better positioned to weather the economic confrontation. The severity of Scenario 1 emphasizes China’s acute sensitivity to external trade measures, while Scenario 4 reflects the devastating long-term consequences of systemic decoupling.

Scenario 1: Targeted Trade Shock with Unexpected Severity

Scenario 1, involving the removal of China’s Most-Favored-Nation (MFN) status, imposes an unexpectedly severe trade shock on China. While China’s GDP decline is modest at -0.02%, the impacts on exports (-6.14%) and imports (-10.52%) are disproportionately large, revealing China’s acute sensitivity to external shocks, particularly in trade flows. This leads to a significant increase in the trade balance (¥636.33 billion), driven by collapsing imports rather than healthy economic activity. Social welfare shrinks by ¥119.06 billion, signaling domestic economic distress. For the U.S., the impacts are more neutral, even mildly positive. GDP grows by 0.06%, with reductions in exports (-7.81%) and imports (-8.37%) reflecting broad trade adjustments. The trade balance improves by ¥629.4 billion, and social welfare posts a modest gain of $17.19 billion, highlighting the U.S.’s initial resilience in managing the disruptions.

Scenario 2: Broad Tariffs with Moderate Impacts

Scenario 2 spreads economic pressure across all trade partners through a universal 10% tariff, which avoids singling out China. For China, GDP contracts to -0.09%, while exports fall by -2.96% and imports decline by -5.08%. Although China’s trade balance improves by ¥308.82 billion, this growth reflects shrinking trade volumes rather than economic strength. Social welfare losses moderate slightly to ¥54.75 billion, compared to Scenario 1. For the U.S., this broader tariff strategy brings moderate disruptions. GDP grows by 0.03%, and exports (-3.63%) and imports (-4.07%) decline. The trade balance improves by ¥339.3 billion, and social welfare posts a smaller gain of ¥14.43 billion.

Scenario 3: Significant Dual Trade Pressure

Scenario 3 combines the removal of MFN status with a global 10% tariff, amplifying economic pressure on China. The effects become significant across all key metrics: China’s GDP contracts by -0.12%, while exports drop sharply by -9.34% and imports plunge to -16.03%. This severe contraction leads to a substantial increase in the trade balance (¥973.68 billion), as imports collapse. Social welfare losses escalate to ¥174.44 billion, reflecting the cumulative domestic burden of trade disruptions. The U.S. experiences similarly sharp trade contractions. GDP rises modestly by 0.07%, but exports fall by -11.8% and imports drop by -12.92%. The trade balance improves notably to ¥1024.33 billion, and social welfare gains increase to ¥20.8 billion.

Scenario 4: Systemic Economic Stress and Near Collapse

Scenario 4 represents the worst-case outcome, applying an extreme 60% tariff on Chinese imports alongside a 10% global tariff on other trade partners. For China, this leads to systemic economic stress. GDP contracts sharply by -0.43%, while exports collapse (-18.21%) and imports nosedive (-31.38%), signaling near-paralysis of trade activity. The trade balance grows to ¥1926.01 billion, but this reflects an economy crippled by collapsing imports. Social welfare losses peak at ¥317.69 billion, demonstrating immense economic hardship. For the U.S., while trade disruptions are severe, the economy shows resilience. GDP increases to 0.14%, but exports fall significantly by -21.9% and imports decline by -25.25%. The trade balance improves dramatically to ¥2230.23 billion (about $312 billion at 7.3¥/$), but the underlying economic strain remains. Social welfare gains taper off to ¥15.49 billion, suggesting diminishing returns from trade disruptions.

4. Which Scenarios to expect under Trump 2.0: Scenarios 1 and 4

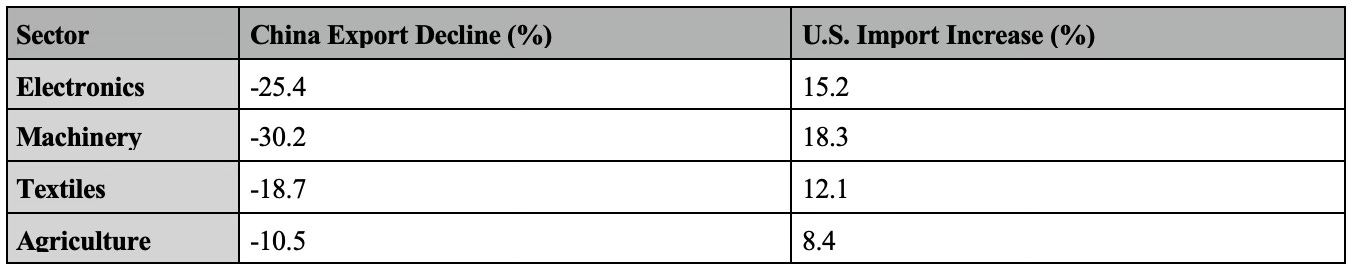

Generally, the four scenarios reveal a non-linear progression in their economic impacts on China. Scenario 1—though seemingly mild—hits China’s trade and social welfare harder than expected, underscoring its vulnerability to targeted shocks like the removal of MFN status. As the scenarios escalate, the impacts broaden to affect China’s GDP more severely, with Scenario 4 ultimately delivering the most severe trade and domestic welfare losses. The sectoral impacts of Scenario 4 are particularly striking, as shown in Table 5 below. Key sectors such as electronics and machinery – pillars of China’s industrial strength – experience significant export declines, with ripple effects on the U.S. import landscape.

In contrast, the U.S. demonstrates relative resilience across all scenarios. While trade contractions intensify, the U.S. economy maintains modest GDP growth and benefits from improvements in its trade balance. Social welfare gains, though diminishing in later scenarios, highlight the U.S.’s ability to adapt, even as trade protectionism escalates globally.

To maximize harm to China while minimizing the damage to the U.S. economy, the most likely and effective strategy under Trump 2.0 is a combination of Scenario 1 (MFN Revocation) and Scenario 4 (Extreme Tariffs), should Trump2.0 focus on manipulating trade dynamics through tariffs and MFN revocation rather than addressing macroeconomic fundamentals.

Targeted Decoupling: MFN revocation isolates China’s economy, forcing companies to shift supply chains away from China, leading to long-term structural damage.

Systemic Pressure: Extreme tariffs cripple China’s key industries and suppress its export dominance, exacerbating domestic economic challenges.

U.S. Trade Balance Gains: Both scenarios dramatically improve the U.S. trade balance by curtailing imports, while GDP remains stable or modestly positive.

From a macroeconomic perspective, this approach:

Manipulates trade balances artificially to offset structural deficits without addressing domestic savings shortfalls.

Forces China into policy adjustments (e.g., subsidies, devaluation) that could further weaken its economy.

Minimizes immediate harm to U.S. GDP and social welfare, sustaining Trump’s domestic political narrative of economic resilience.

While the trade imbalance with China may narrow under these scenarios, the overall U.S. trade deficit is unlikely to improve and could worsen due to trade diversion to other countries and higher domestic costs.

In contrast, scenarios 2 and 3 are less likely. These scenarios may hurt the global economy but are less likely to align with Trump’s objectives of isolating China while boosting domestic perceptions of U.S. strength.

Scenario 2 (Global Tariff) spreads economic costs across all U.S. trade partners, introducing broad inflationary pressures domestically. While it avoids singling out China, the uniform 10% tariff raises costs on imported goods, disproportionately affecting U.S. consumers and businesses.

Scenario 3 (Dual Pressure) combines MFN revocation with global tariffs, amplifying inflation risks further. By targeting Chinese goods while simultaneously raising costs for imports from other countries, this scenario delivers significant economic disruption to China but introduces sharp price increases in essential goods for the U.S. market, complicating Trump 2.0’s domestic objectives.

5. China’s Potential Countermeasures and Strategic Adaptation

China is likely to adopt a multi-pronged strategy, combining defensive economic policies with proactive global engagement. Key elements include:

Policy Adjustments: Utilizing tariff policies, export controls, currency devaluation, and subsidies to stabilize affected industries.

Trade Negotiations: Strengthening second-track diplomacy and leveraging middle-power alliances to counter U.S. isolationist strategies.

Market Diversification: Expanding into emerging markets, though the diminishing returns of external demand pose challenges.

Multilateralism: Deepening institutional integration in global trade systems, such as RCEP, to offset U.S.-led disruptions.

Domestic Stability: Prioritizing internal economic reforms, accelerating technological self-sufficiency, and boosting domestic consumption to reduce reliance on external markets.

Based on the four scenarios and their impacts, China’s response will likely combine short-term stabilization and long-term structural adjustments.

Immediate Responses: In scenarios like Scenarios 1 and 4, China will prioritize policy adjustments (currency devaluation, subsidies) to stabilize exports and key industries.

Global Engagement: Scenarios 2 and 3, which involve broader tariffs, necessitate proactive trade negotiationsand multilateral cooperation to strengthen alliances and mitigate isolation.

Structural Resilience: In the worst-case Scenario 4, domestic reforms, technological self-sufficiency, and efforts to boost domestic consumption become even more critical to reducing reliance on external markets; however, alternative markets have already been largely exhausted for the time being.

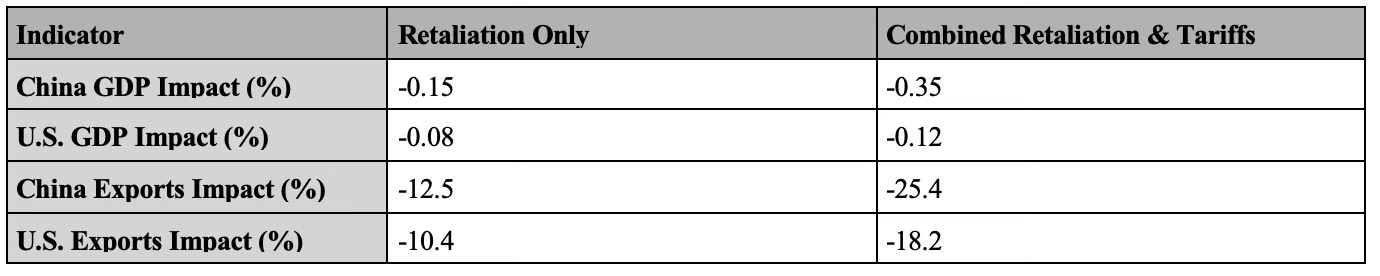

As highlighted through the impact of the scenarios, China’s potential retaliation to U.S. trade policies under Trump 2.0 presents a double-edged sword, as highlighted above. While such measures aim to counteract the economic pressure imposed by U.S. tariffs, they also risk exacerbating trade and economic disruptions for both nations, ultimately disadvantaging China. The table below quantifies the effects of China’s retaliation under two scenarios: retaliation alone and combined retaliation with U.S. tariffs.

The table illustrates the asymmetric economic impacts of China’s retaliation under two scenarios. While both nations experience economic disruptions, China faces disproportionately severe consequences. GDP declines are steeper for China, ranging from -0.15% under retaliation alone to -0.35% under combined retaliation and tariffs, compared to the U.S.’s more moderate declines of -0.08% to -0.12%. Export losses are similarly lopsided, with China’s exports dropping -12.5% to -25.4%, significantly outpacing U.S. export declines of -10.4% to -18.2%. This underscores the mutual harm caused by trade wars, but it also reveals China’s heightened vulnerability due to its export-dependent economy and limited alternative markets.

Summary and Concluding Thoughts

Under the Trump 2.0 administration, according to Professor Liu Yuanchun’s analysis and interpretations, the U.S. is expected to escalate its economic confrontation with China through a combination of coercive measures. While tariffs remain a central feature of the strategy, the Chinese government expects a broader set of tools targeting financial markets, advanced technology, and global supply chains. This reflects a strategy aimed at systemic decoupling, leveraging both direct trade actions and more complex economic disruptions. By no means can China rely on a “transactional Trump” or a “peaceful Trump.”

Tariffs are expected to remain a central feature of U.S. economic measures against China under Trump 2.0, as illustrated by the scenarios. Strategies such as revoking China’s Most-Favored-Nation (MFN) status and imposing tariffs as high as 60% on key sectors like electronics, machinery, and textiles are designed to undercut China’s export-driven industries while appealing to domestic constituencies in the U.S. While Scenario 1 and Scenario 4 stand out as having the most severe impacts on China—highlighting its disproportionate vulnerability to trade shocks—the inflationary repercussions and domestic costs in the U.S. could complicate the implementation of these strategies, particularly when balancing economic and political objectives.

Beyond tariffs, expanded measures could target financial markets, state-owned enterprises, and critical technology exports. These tools reflect the evolving nature of U.S.-China competition, which increasingly focuses on long-term strategic vulnerabilities rather than immediate trade flows. While evidence of a definitive shift away from tariffs is limited, the broader framing of “national emergency” and "national security" in U.S. trade policy suggests an escalation across multiple domains.

China’s economic resilience will be tested by this multifaceted approach. Vulnerabilities in supply chains, technology dependencies, and export reliance present significant challenges. Analysts emphasize the importance of domestic economic reforms, technological self-sufficiency, and enhanced global cooperation through mechanisms like RCEP and WTO frameworks to mitigate the impacts of U.S. actions. For China, Trump 2.0 requires a recalibration of both domestic and international strategies to strengthen resilience against a more comprehensive and sustained confrontation. The evolving U.S. approach signals a more complex and protracted phase of economic and geopolitical rivalry. Once Trump’s measures become implemented, it will become clearer how China mitigates these actions, engages in mutual risk hedging with Europe as a form of collaboration, and further refines the allocation of its first major post-COVID stimulus package. These measures might accelerate China’s shift towards a more consumption-led economy rather than an export-driven one, while simultaneously pushing for greater self-sufficiency and technology innovation. Some of these strategic responses are likely to influence China’s upcoming 15th Five-Year Plan (2026–2030). In the end, however, macroeconomic constraints and the dollar conundrum–factors the U.S.- administration cannot easily manipulate–could tame America’s “neo-Manifest Destiny” and prevent Trump’s wildest ideas from materializing, ultimately forcing the new administration into a more transactional approach. Neither Trump 1.0 nor the Biden-Harris administration has managed to contain China. Indeed, the contradictions of the "small yard, high fence" strategy have proven to be a “fool’s errand.” Trump’s statement that “China and the United States can together solve all of the problems of the world” may hint at a potential policy shift towards a wold that is tired of (trade) wars.